Aussie Gains Second Week, Nears January Highs Versus Dollar

Swaps traders bet yesterday that the Reserve Bank of Australia will raise its benchmark rate by 1.17 percentage point over 12 months, from 89 points on March 5, according to a Credit Suisse AG index.

The Reserve Bank of Australia raised the benchmark rate March 2 and Assistant Governor Philip Lowe said March 10 that the nation's economy will expand at or above its average pace over the next couple of years.

"Upward pressure on interest-rate expectations in the wake of the decision suggests policy makers expressed more confidence in the economic pick-up than anticipated," New York-based Todd Elmer and London-based Michael Hart, strategists at Citigroup Inc. wrote in a note to clients yesterday. The bank expects the RBA's next increase in June with one percentage point of advances by year's end.

Benchmark interest rates are 4 percent in Australia and 2.5 percent in New Zealand, compared with 0.1 percent in Japan and as low as zero in the U.S., attracting investors to the South Pacific nations' higher-yielding assets. The risk in such trades is that currency market moves will erase profits.

Eoin Treacy's view Australian interest rates

have risen 1% since September but are still 0.25% below the lowest level seen

since the early 1970s, so current policy can be characterised more as removing

stimulus rather than tightening.

The Australian

Dollar regained the majority of its bear market decline by November but

by that that stage had become comparatively overextended relative to its mean,

defined by the 200-day moving average. It has been ranging with a mild downward

bias since and found support at the mean in February. It continues to rally

towards the January high and a sustained move above 93¢ would indicate

a return to more demand dominated environment. .

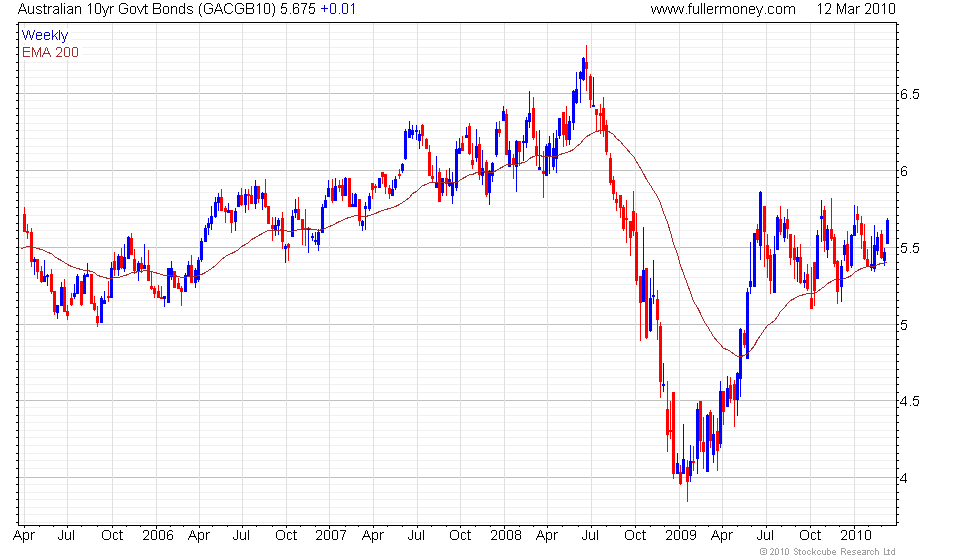

The Australian

10yr bond is beginning to price in future inflation. Yields

bottomed out near 4% in January 2009 and quickly rallied to 5.8%, below which

it has been consolidating since June. The 9-month range has developed a rounding

characteristic which is consistent with a return to demand dominance for yields.

A sustained move below 5.35% would be required to question scope for further

upside.

The Canadian

10yr has a similar pattern and a sustained move below 3.3% would be required

to question scope for higher to lateral ranging. The Singapore

and New Zealand yields share a similar

trajectory.

UK

government bond yields are also pushing higher but for somewhat different reasons.

While the Australian and Canadian economies have come through the financial

crisis comparatively well, the UK has made little effort to trim deficits and

has allowed the Pound to absorb much of the negative sentiment towards the economy.

The Gilt market is not also attracting investor attention and higher yields

are being demanded for accepting the increased credit risk presented by the

UK. The 10yr yield broke back above 4% in February and found support at that

level again last week. A sustained move back below 3.85% would now be required

to question scope for further higher to lateral ranging.

Elsewhere,

the German 10yr yield continues to trend

lower and would need to sustain a move above 3.3% to question scope for further

lower to lateral ranging.

{kind=link}