Deepak Lalwani's India Report

ECONOMIC NEWS

The Indian Rupee has appreciated about 7% this year vs a near 16% fall in 2011 when it ended the year at Rs 53.01 vs the US$. With poor economic data signalling a sharply decelerating economy, at the start of 2012 a fall to Rs 55 was possible in January. And, a possible further depreciation down to Rs 60 vs the US$, as markets often overshoot. However, what caused the reversal of trend was the unexpected sharp fall in food inflation (in fact it turned to food deflation for the first time in 6 years). This in turn triggered a sharp fall in wholesale inflation to 7.47% for December 2011, the lowest for 2 years. This raised hope that interest rates, which had risen 13 times in 2010 and 2011, had peaked. And, that the next move would be downwards, possibly as early as March, if inflation is in the 6.5 - 7.5% range for the next two readings. FIIs sensing a turnaround in the economy if interest rates are cut, have invested an impressive $ 2.08 bn in Indian shares this month, after being net sellers of $ 348m in all of 2011. The strong capital inflows from FIIs, coupled with US$ weakness, has helped the Rupee claw back in one month almost half of its loss for all of 2011. Further appreciation is expected this quarter to around Rs 48 vs the US$ as Indian shares regain attraction for foreign investors, leading to further capital inflows.

David Fuller's view A downturn in food

price inflation and a firmer currency is very welcome news for India and

I hope the RBI follows with a series of rate cuts. They would cushion downside

risk for the economy and eventually lead to a stronger phase of GDP growth.

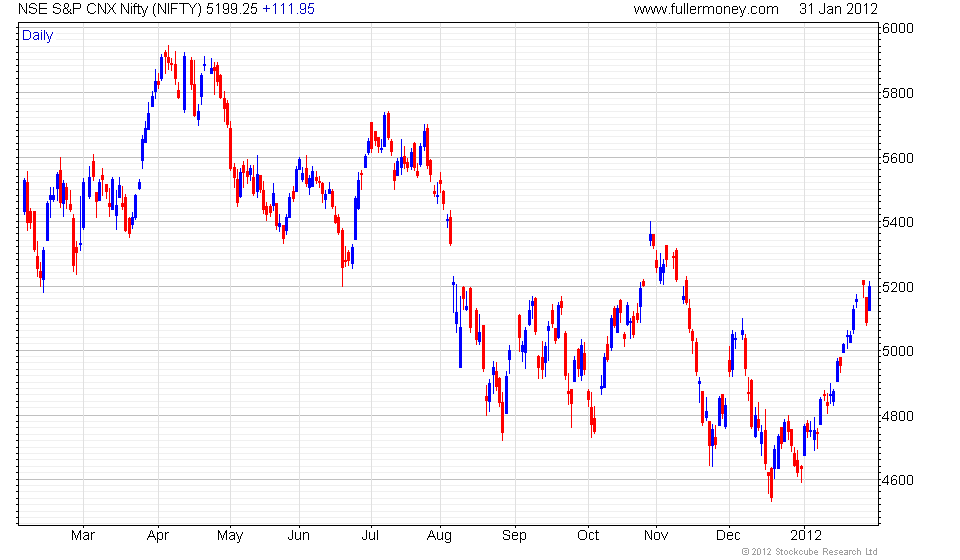

India's

stock market (weekly & daily)

has tested investors' patience since its peak in November 2010, not to mention

the numerous problems of governance. Nevertheless, with expectations low any

favourable news can lead to outperformance as we have seen recently. For this

to last we need to see resilience during a consolidation of recent strong gains,

followed by a break in the medium-term downward trend, requiring a sustained

push above the late-October rally high.

{kind=link}