Japan Strategy The Relevance of Japan: Everything to Play for�.

Should Japan attempt a policy of austerity in one country, the risk is open-ended yen appreciation. It seems to us unlikely that policy-makers would be willing to run such risks.

Far easier to allow oneself to be drawn towards the combination which always worked before - domestic fiscal stimulus, with the central bank cooperating to offer some monetary accommodation as well - a combination that might be seen as the diplomatic price to be paid for foreign acquiescence in a lower-than-otherwise external value for the currency. This is exactly the combination that now appears to be developing.

In addition, the scale of the damage done to the stock market by the global meltdown has provoked renewed interest in the question of banks' balance sheet exposure to equities. In 2003, financial pressures resulted in one bank having publicly-quoted equities stripped entirely from its balance sheet; all the banks found new limits placed on their equity exposure.

This theme has returned, with both the BoJ and the Bank Shareholding Purchasing Corporation authorized to buy bank held equities. The total value of their budgetary authorization is ¥21 trillion - over 10% of market capitalization and more than the aggregate holdings of the banking sector.

While we emphasise the primacy of macro factors, we can conceive of no individual improvement to Japan's financial sector of greater importance to the character and valuation of the stock market than to eliminate banks' exposure to equities. By 2014 bank ownership of public equities will in any case become effectively impossible if changes to BIS regulations are enacted as currently proposed. Reduction in the banks' arguably excessive exposure to risky equities, and the excess volatility this engenders in the credit cycle, could allow for a fall in the risk premium attached to the whole market. That this discussion has surfaced now is, perhaps, an unlooked for positive arising out of global events.

Eoin Treacy's view While the USA and Europe are not tightening, they are allowing some of the extreme policy measures implemented since Q32008 to expire and are talking about how best to begin to normalise policy. Japan is not at that stage just yet and policy remains extremely accommodative. At the very least, we can expect that a strong Yen is something the authorities will seek to avoid.

The Euro found support against the Yen on Thursday in the region of ¥123 and continues to rally. A sustained move below that level would be required to question potential for additional upside. Against comparatively stronger currencies such as the Korean Won, the Yen remains weak, with the Won holding the recent breakout. A sustained move back below ¥8 would be needed to begin to question medium-term upside potential. We continue to believe that a weak Yen was the missing catalyst needed to spur investor interest in Japan. Recent stock market action supports this view.

The stock market is not expensive and could be viewed as cheap on measures such as Price/Book or perhaps more importantly in price terms and relative to the 1989 peak. Being a doubter of Japan's long-term potential has paid off over the last 20 years and has become the accepted view of the market. Even Japan bulls are cautious about extrapolating beyond the short term and I am increasingly becoming of the opinion that the maxim "those who know it best, love it least because they have been disappointed the most" is apt for Japan.

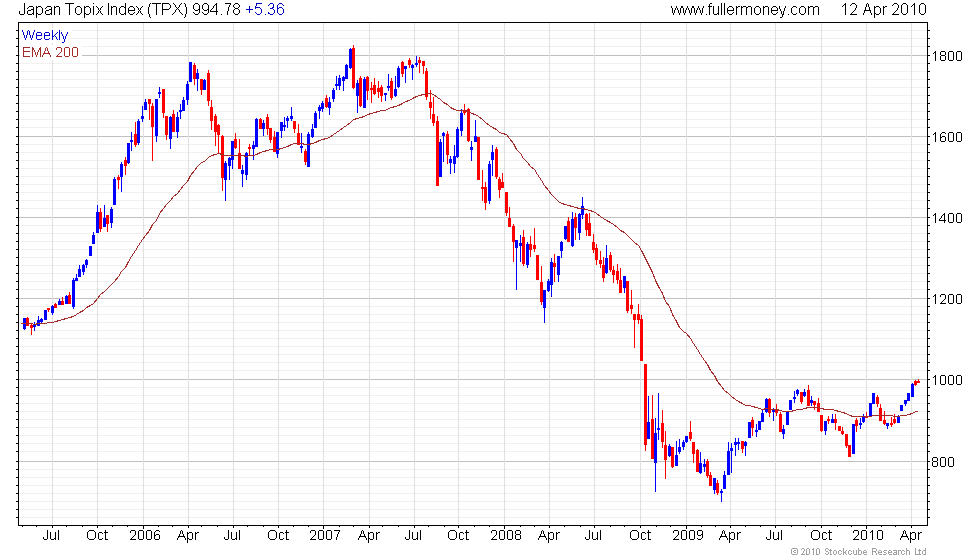

The Topix Index has been forming a base since 1992. It found support in the region of the 2003 lows last year and has been ranging below 1000 since August. The Index is now testing that level once more and a sustained move above it would further emphasise the fact that bullish interest it returning to dominance.

The Topix Banks Index also found support in the region of the 2003 lows and has been rallying of late. I broke upwards from the six-month range earlier this month and last week moved back above the 200-day moving average for the first time since June. A downward dynamic would be required to question the short-term advance while a sustained move to new lows would be required to delay medium-term recovery potential.

Japan has been a serial disappointment for investors over the last two decades and it would be rash to say that the deflationary spectre has been banished. However, the apparent risk versus the potential reward favours the market over the medium-term.

{kind=link}