Sugar Gains in London as Goldman Sachs Raises Price Forecasts

Sugar rose in London as Goldman Sachs Group Inc. predicted higher prices for the sweetener on concern about global harvests.

The bank increased its three-month price forecast for raw sugar to 20 cents a pound, analysts led by London-based Jeffrey Currie wrote in a report today. Goldman Sachs boosted its six- and 12-month estimates to 16 cents from 12 cents. Raw sugar headed for a sixth weekly gain in a row in New York.

"Uncertainty over the 2010-11 crop will likely become the main driver for sugar prices over the coming months," the analysts said. "Adverse weather over the past months points to lower-than-previously-expected production for both Brazil, the largest producer and exporter, and Australia, the third-largest exporter."

White, or refined, sugar for December delivery gained $7.40, or 1.2 percent, to $615.60 a metric ton at 9:41 a.m. on NYSE Liffe. The contract climbed for a 13th day in 14.

Pakistan yesterday formed a panel to report on sugar imports to ease a shortage estimated at 1.2 million tons next year. The panel will make its assessment on overseas purchases within a week, the Industries Ministry in Islamabad said in a statement yesterday. Floods destroyed 200,000 acres of sugar cane, a farm group in the South Asian nation said last month.

Eoin Treacy's view Sugar

prices have been recovering over the last few months in a steady progression

of higher reaction lows. The US traded contract is a little overbought in the

short-term but has held above 20¢ since September 2nd and a sustained move

below that level would be required to question the consistency of the short-term

uptrend. A decline below the 200-day MA, currently in the region of 18.75¢,

would be required to question medium-term upside potential.

Against

a background of appreciating soft commodity prices, companies leveraged to higher

food prices such as fertiliser producers or those with the ability to pass on

input prices hikes such as some food processors are likely to attract investor

interest. Tate & Lyle caught my attention earlier

this week because it appeared in the list of European shares that had increased

dividends every year for the last consecutive 10-years. It currently yields

4.95% and while it had a poor last quarter which saw its P/E soar, the estimated

P/E is back down to a more reasonable 11. If earnings come in as expected the

dividend cover and payout ratios should also fall back into line.

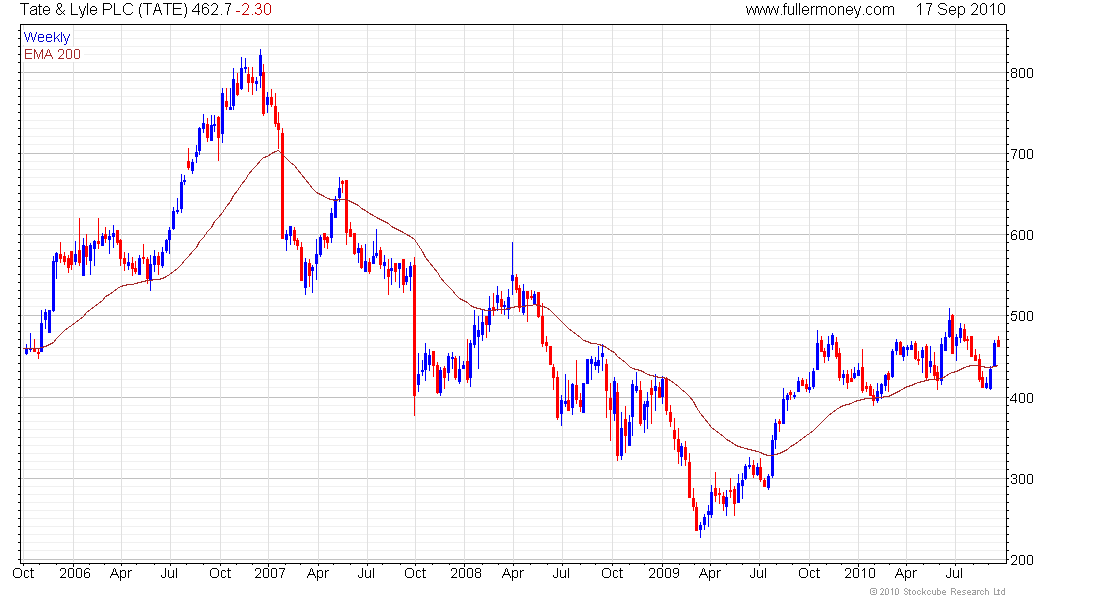

The share

did very well back in 2006 as sugar prices rallied on increased ethanol production

but failed to benefit from the subsequent performance of the commodity and posted

a progression of lower rally highs for more than 2 years. It broke this sequence

in August 2008 and be ranging mostly above 400p since. It is currently rallying

from the lower side of this range and a sustained move above 500p will reaffirm

the medium-term uptrend.

This

article by Hannah Kuchler

for the Financial Times dated July 1st indicates that Tate & Lyle have sold

their sugar manufacturing operations to concentrate on their core speciality

ingredients section of which sugars and sweeteners are a major part. I have

no additional information on whether this will allow the company to pass on

higher input prices to its customers but the chart action suggests this may

be the case.

{kind=link}